Droit Fiscal Américain

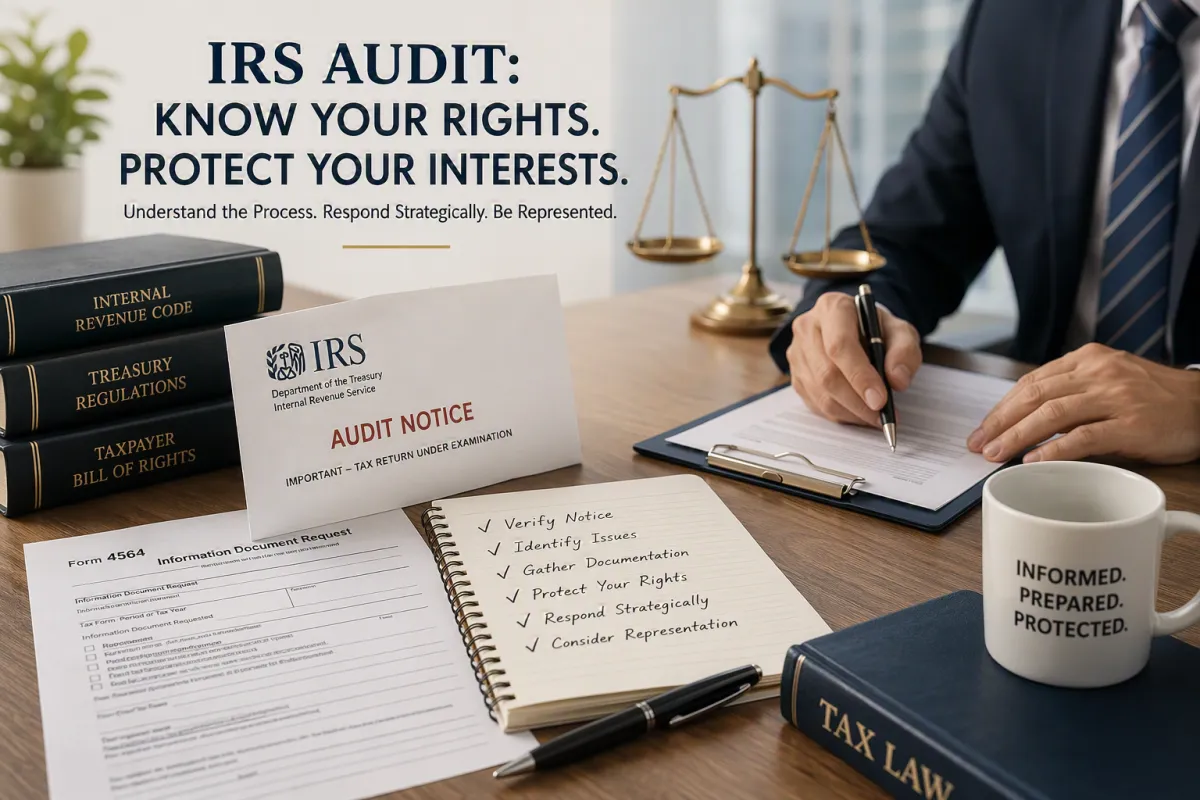

IRS Audit: Know Your Rights, Control the Process, and Protect Your Interests

A concise guide to IRS audits: how they begin, your taxpayer rights, and when to involve a tax attorney to protect your position and control the process effectively.

Doing Business in the U.S. Without a Physical Presence: A Guide for Foreign E‑Commerce Companies

Foreign e‑commerce companies can access the U.S. market without a physical presence. This article explains how a U.S. LLC, careful structuring, and tax treaty rules can help limit exposure to U.S. taxation.

ROBINSON THABUKO

Unauthorized LinkedIn affiliation: THEVOZ Attorney LLC clarifies that Mr. Robinson Thabuko has no connection to the firm and that corrective actions have been initiated.

Streamlined Filing Compliance Procedures IRS

Understand the key difference between non-willful conduct and reasonable cause in U.S. offshore compliance—and why proactive Streamlined filings can significantly reduce IRS penalty exposure compared to an audit scenario.