Droit Fiscal Américain

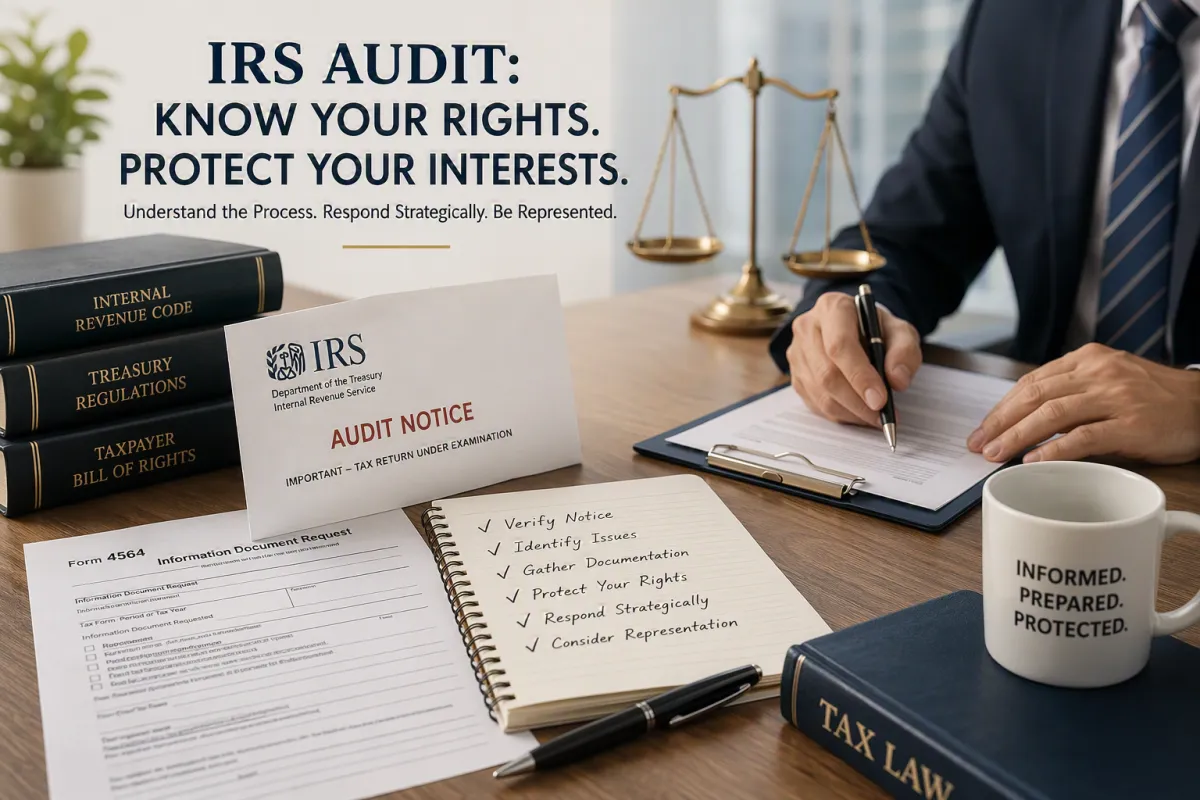

Contrôle fiscal IRS : connaître vos droits, maîtriser la procédure et protéger vos intérêts

Guide pratique du contrôle fiscal IRS : déroulement, droits du contribuable et rôle de l’avocat fiscaliste pour sécuriser les échanges, maîtriser la procédure et réduire les risques.

IRS Audit: Know Your Rights, Control the Process, and Protect Your Interests

A concise guide to IRS audits: how they begin, your taxpayer rights, and when to involve a tax attorney to protect your position and control the process effectively.

Fiscalité américaine et absence de présence physique : guide pour les entreprises étrangères de e‑commerce

Découvrez comment une entreprise étrangère peut vendre aux États‑Unis sans présence physique, via une LLC, tout en limitant son exposition à l’impôt américain grâce à une structuration adaptée et aux conventions fiscales.

Doing Business in the U.S. Without a Physical Presence: A Guide for Foreign E‑Commerce Companies

Foreign e‑commerce companies can access the U.S. market without a physical presence. This article explains how a U.S. LLC, careful structuring, and tax treaty rules can help limit exposure to U.S. taxation.